Last Updated

Quick Summary

The børneopsparing is Denmark’s only investment account where all returns are completely tax-free: no capital gains tax, no income tax, nothing. For the duration of the binding period. Relevant to expats with children who are Danish tax residents. The account must be opened before the end of the calendar year the child turns 14. The annual deposit limit is DKK 6,000, with a lifetime deposit cap of DKK 72,000. Growth does not count toward the limit.

The børneopsparing is the only account in Denmark where investment returns (interest, dividends, and capital gains) are completely tax-free. No income tax, no capital gains tax, nothing. In a country where investment returns are normally taxed between 17% and 42%, that matters. This guide is for expats who’ve decided to open one and want to get it right.

The Rules at a Glance

| Rule | Detail |

| Who can open it | Parents, grandparents, great-grandparents, step-parents, adoptive parents |

| Age limit to open | Before the end of the calendar year the child turns 14 |

| Accounts per child | One. A second account won’t be tax-free. SKAT’s systems will catch duplicates. |

| Annual deposit limit | DKK 6,000 |

| Lifetime deposit limit | DKK 72,000 (growth doesn’t count toward this) |

| Minimum binding period | 7 years from opening |

| Payout window | Earliest: child turns 14. Latest: end of the calendar year child turns 21. |

| Tax on returns | Zero. All returns are tax-free during the binding period. |

| Gift tax | Deposits count toward the tax-free gift threshold (—/giver in 2026). |

Tip

One account per child. Open it before the year they turn 14. All returns are tax-free until the binding period ends.

How to Open One

You can’t open a børneopsparing at Nordnet, Saxo Bank, or any online-only platform. It must be a traditional Danish bank: Danske Bank, Nordea, Jyske Bank, Sydbank, Nykredit, or similar. You’ll need the child’s CPR number, a birth certificate or personattest, the child’s sundhedskort, and your own MitID. Most banks handle everything through netbank or mobilbank.

Ask specifically for a børneopsparing, not a “child’s savings account” or “gavekonto,” which are different products with different tax treatment. Choose your binding period (14, 18, or 21), decide whether to invest or hold cash, and set up a standing order of DKK 500/month. Then automate and forget.

Choosing a Bank

The most important question: does the bank let you invest the money yourself, or does it force you into pooled products?

Self-directed depot (børneopsparingsdepot): You pick your own funds, ETFs, and stocks via netbank. Full control, access to low-cost index funds. Offered by Danske Bank, Jyske Bank, Nordea, Sydbank, and most larger banks.

Puljeinvestering (pooled products): The bank invests in its own funds. You choose a risk profile; they do the rest. The problem is cost: pool fees typically run 0.75-2% annually. As of 2026 Danske Bank’s pools charge around 2.02% per year; Jyske Bank’s around 1.87%. Compare that to a passive index fund at 0.1-0.5%. Over 21 years, the difference can strip out 30% of your total returns.

Cash only: Just earns interest. Even at the best rates, cash will almost certainly underperform invested børneopsparinger over a 12-21 year horizon.

Tip

Choose a bank with a self-directed depot. Ask directly: “Can I choose my own investeringsforeninger and ETFs, or am I limited to puljeinvestering?” If pools only, consider a different bank. You can transfer the børneopsparing later, but it involves paperwork and potentially a fee.

What to Invest In

The børneopsparing’s tax-free status changes the investment logic entirely. In a normal depot, you’d worry about Positivliste status, aktieindkomst vs. kapitalindkomst, and accumulating vs. distributing. Inside the børneopsparing, none of that matters. Optimise for the best risk-adjusted returns at the lowest cost.

- Go 100% equities. With 12-21 years and no ability to withdraw early, you have time to ride out volatility.

- Use a broad, low-cost global index fund. A single fund tracking the MSCI World or FTSE All-World gives diversification across 1,500+ companies. Target ÅOP under 0.5%.

- Danish investeringsforeninger work well here. Buying Danish-domiciled funds through a Danish bank depot avoids foreign dividend withholding complications.

- Minimise trading. Bank kurtage is typically DKK 29-99 per trade. With DKK 6,000/year flowing in, buy once or twice a year rather than monthly.

- Individual stocks are allowed but risky. Some banks cap single-issuer exposure at 20% of the balance or two years’ deposits. With small annual amounts, concentration risk is high. Stick with diversified funds.

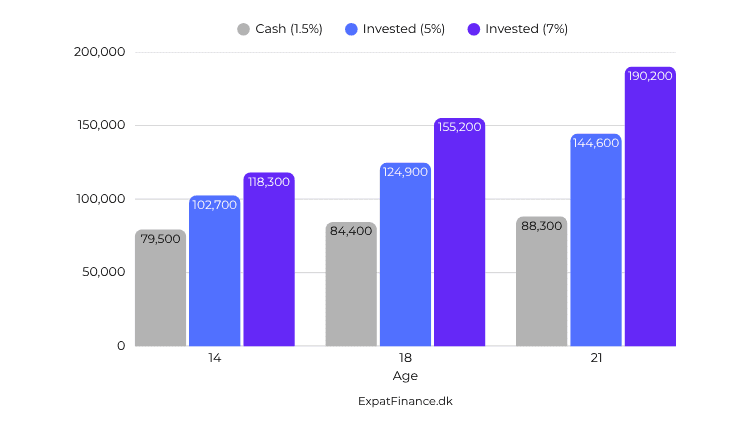

The Maths: Cash vs. Invested

Depositing DKK 6,000/year from birth for 12 years (DKK 72,000 total), then letting it compound:

At 7%, your child receives roughly DKK 190,200 at age 21, DKK 118,200 in pure tax-free growth. In a taxable account, you’d lose 27-42% of those gains. Even starting late matters: opening at age 7 and depositing for 7 years at 5% still yields roughly DKK 68,000 by age 21, nearly DKK 26,000 in tax-free growth.

Tip

The tax-free status is most valuable when the money is invested for a long time. Cash earns interest; equities, over 12-21 years, are likely to do considerably more.

Binding Period: 14, 18, or 21?

Until 14: The parent controls the money (the child is still a minor) and must use it in the child’s interest. Common uses: efterskole fees, confirmation costs.

Until 18: The child gets full control at 18. Parents have no say from that point.

Until 21: Three extra years of tax-free compounding, worth roughly DKK 35,000 at 7% returns. The child gets control at 21.

You can extend the binding before it expires (the new period must be 7+ years, and can’t go past age 21). You can’t shorten it once set. If you’re opening at birth, the arithmetic favours choosing 21. You maximise growth and can always revisit before the child turns 14.

When the Binding Period Ends

The bank converts the account to a regular savings account. The tax-free status ends immediately. From that date, all new returns are taxable in the child’s name under normal rules.

There’s an important exception: if the original deposits came from parents (not grandparents), interest and dividends after binding are taxed in the parent’s name until the child turns 18. Capital gains stay with the child regardless.

Don’t leave a large invested balance sitting in a newly taxable account without a plan. The two main options: move funds to an aktiesparekonto (flat 17% tax rate), or restructure into kapitalindkomst funds that stay within the child’s personfradrag (DKK 54,100 in 2026).

Six Mistakes Expats Make

- Confusing fintech products with the real thing. Services like Tobi are regular depots using the child’s personfradrag, not a børneopsparing under PBL § 51. The personfradrag shelter collapses once the child gets a part-time job. A genuine børneopsparing stays tax-free regardless.

- Trying Nordnet or Saxo Bank. Neither offers a børneopsparing. Their “depot for mindreårige” is a different, taxable product.

- Missing the age-14 deadline. You must open before the end of the calendar year the child turns 14. No exceptions, no backdating.

- Opening two accounts. Only the first is tax-free. SKAT’s systems will catch duplicates.

- Leaving money in cash. Around half of Danish børneopsparinger sit in cash. Over 21 years, the difference between cash and invested is potentially DKK 50,000-100,000 in forgone tax-free growth.

- Ignoring pool fees. Puljeinvestering at 1.5-2% annual costs is a significant hidden drag on a nominally tax-free account. Always check the ÅOP before committing.

If You Leave Denmark

The børneopsparing remains tax-free even if you leave. It’s not subject to Danish exit taxation. The binding period runs as normal.

Check whether your new country taxes the returns. Most don’t have an equivalent concept. The børneopsparing is separate from your ASK and free depot, which are subject to exit-tax rules.

Coordinating with Grandparents

The DKK 6,000 annual limit applies per account, not per depositor. If parents and grandparents both contribute, their combined deposits can’t exceed that figure. The bank moves any excess to a regular account.

A cleaner approach: parents fill the børneopsparing. Grandparents direct their money to a frit depot in the child’s name instead. Grandparent-gifted money in a depot is taxed in the child’s name, meaning it can use the personfradrag for an effective 0% rate on kapitalindkomst up to DKK 54,100/year. Each grandparent can give DKK 80,600/year (2026) tax-free.

Can You Move the Børneopsparing?

Yes. The person who opened the account (the indskyder) can request a transfer to another bank. The new bank handles the process. Be aware: the old bank may charge a transfer fee, and investments may need to be sold and repurchased. The binding period and all rules carry over. Nothing resets.

If your current bank only offers expensive pooled products, moving is worth the hassle.

Bottom Line

The børneopsparing is one of the few genuinely good things Denmark’s tax system does for families. Open it early, invest it properly (equities, low-cost funds, self-directed depot), and choose a 21-year binding period if you open at birth. The tax-free compounding does the heavy lifting.

Disclaimer

This article is for informational purposes only and does not constitute financial, tax, or investment advice. Figures reflect publicly available data at time of writing. Always consult a qualified professional regarding your specific situation. See our full disclaimer.